This report is not a personal recommendation and does not take into account your personal circumstances or appetite for risk.

Q4 stocks (2015) page 3

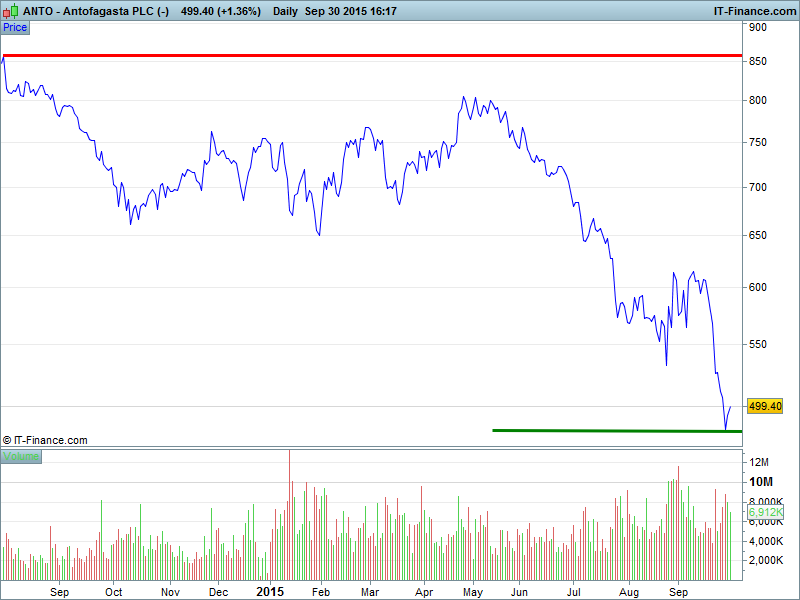

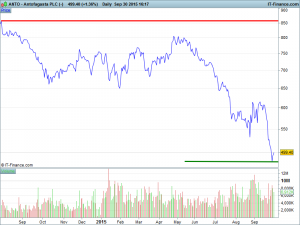

Antofagasta (ANTO)

Copper has received a kick from month-end short covering and more action by the People’s government of China – this time halving sales tax on small cars from 1 Oct, which helped Asian markets rebound at the end of Sept and is widely expected to stimulate car manufacturing in the world’s #2 economy. A subsequent boost in demand for base metals including copper (remember, new cars are highly electronic, if not completely). A modest re-visit of early September levels 615p might be plausible in the short term, especially in what could be a bumper quarter for tech (smartphones, tablets & watches).

ANTO, daily chart (closing prices)

Will shares bounce back to 2015 highs 800p and above? Or will they break down beneath lows of 480p?

Broker Consensus: 16% Buy, 52% Hold, 32% Sell

Most Bullish: Bernstein, Outperform, Target 1025p, +105%

Consensus: Target 623p, +25%

Most Bearish: Berenberg, Sell, Target 352p, -30%

NB: All pricing and consensus data from Bloomberg on 28 Sept; Consensus breakdown available on request

“The UK’s benchmark UK 100 index is recovering, having been under pressure in Q3 from two drivers that are really just one: China”

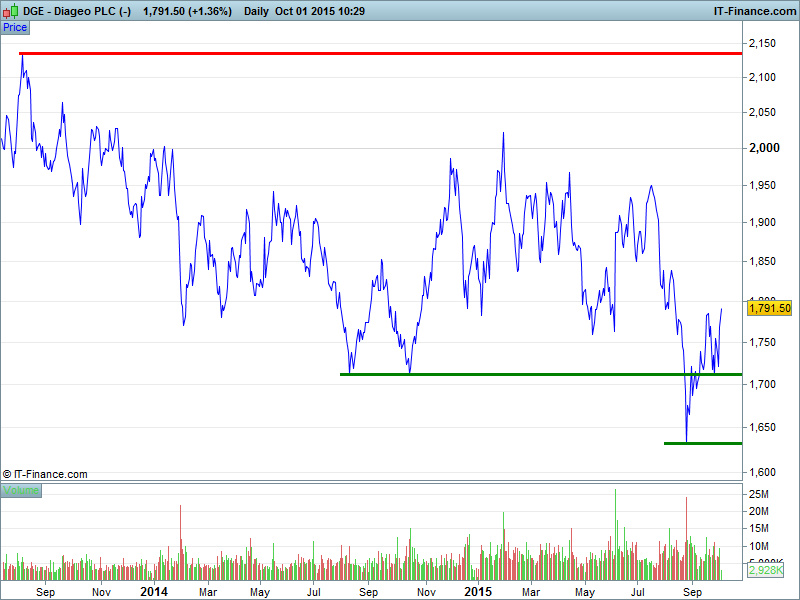

Diageo (DGE)

The drinks maker is putting its underperforming wine business up for sale – a step seen by investors as proactive enough to push shares back into their 2-year trading range after the late August sell-off, which simply exacerbated matters. Granted, a play on a company like Diageo is also a play on China, which has dragged on many a stock of late, but the company is likely to benefit in the medium to long term from its exposure to emerging economies as their growing middle classes seek established drinks brands. Let’s not forget, also, that EM growth rates remain much higher than those of the developed nations, which are already participating fully in a colossal market.

DGE, daily chart (closing prices)

Will shares continue up towards highs of 2140p? Or will they break down beneath support 1710p?

Broker Consensus: 48% Buy, 36% Hold, 16% Sell

Most Bullish: Berenberg, Buy, Target 1300p, +21%

Consensus: Target 1126p, +5%

Most Bearish: SocGen, Sell, Target 930p, -13%

NB: All pricing and consensus data from Bloomberg on 28 Sept; Consensus breakdown available on request

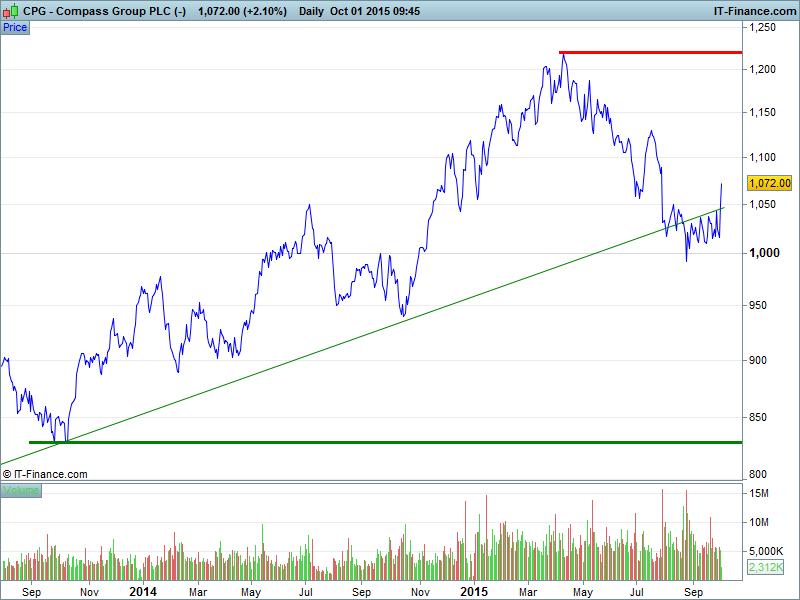

Compass Group (CPG)

Everyone’s gotta eat, right? Compass group is a UK 100 global contract catering and support services company. Revenues across the business of £17.6bn in 2012/13, with £2bn of that in the UK and Ireland alone, have placed CPG in a strong position supporting many sectors – think major Sports, Education, Offshore Oil & Gas and Healthcare. While a likely drawdown in the Offshore & Remote sector due to less oil & gas activity is a concern, we note that Sports related revenue will get a boost from the rugby world cup in Q4 and, of course, income from the Education sector will pick up following the summer holidays. With the recent acquisition of Vision Security Group (VSG) giving clients a fresh alternative to the poorly performing G4S (G4S) in the same package, we think CPG is a great prospect for Q4 trading opportunities.

CPG, daily chart (closing prices)

Will shares continue up towards 2015 highs 1220p? Or will they break down beneath support 1050p?

Broker Consensus: 38% Buy, 48% Hold, 14% Sell

Most Bullish: Berenberg, Buy, Target 1300p, +21%

Consensus: Target 1126p, +5%

Most Bearish: SocGen, Sell, Target 930p, -13%

NB: All pricing and consensus data from Bloomberg on 28 Sept; Consensus breakdown available on request

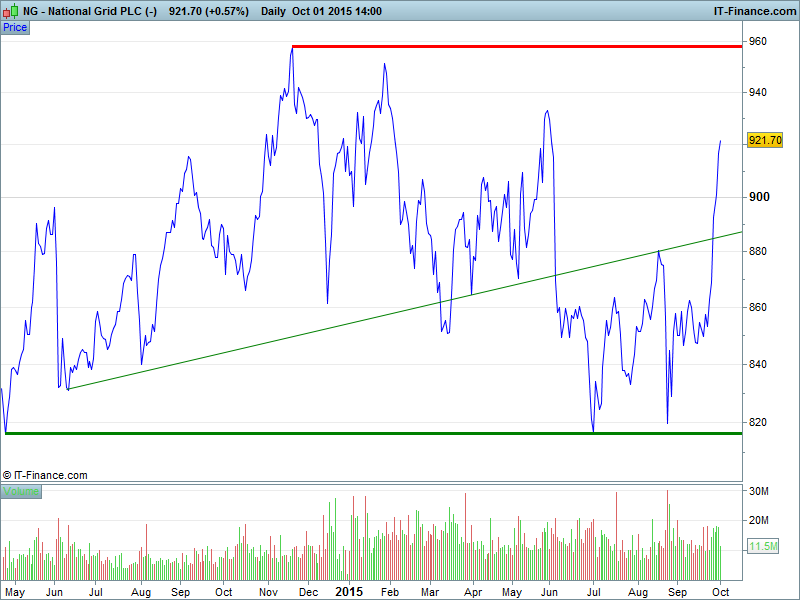

National Grid (NG.)

The income investor can do a lot worse than take a stake in a utility company, and National Grid looks set to be the best bet of the three UK 100 energy providers with an expected dividend yield of 4.9% in the period ending March 2016, and this set to go up to 5% in 2017 – that’s around 45p per share held. NG shares could be the safest of the three in terms of capital returns too, having recovered by an impressive +14% since the 24 August sell-off. While United Utilities (UU.) and Severn Trent (SVT) have also played their defensive roles with aplomb, Centrica (CAN) has continued to slide. In our view, a bet on National Grid is both cheaper than SVT and UU and safer than CNA.

NG., daily chart (closing prices)

Will shares rally towards highs of 958p? Or will they break down towards lows of 816p?

Broker Consensus: 32% Buy, 50% Hold, 18% Sell

Most Bullish: AlphaValue, Add, Target 991p, +8%

Consensus: Target 896p, -3%

Most Bearish: Whitman Howard, Sell, Target 734p, -20%

NB: All pricing and consensus data from Bloomberg on 28 Sept; Consensus breakdown available on request

« Back to Category

This research is produced by Accendo Markets Limited.

Research produced and disseminated by Accendo Markets is classified as non-independent research,

and is therefore a marketing communication. This investment research has not been prepared in accordance

with legal requirements designed to promote its independence and it is not subject to the prohibition on

dealing ahead of the dissemination of investment research. This research does not constitute a personal

recommendation or offer to enter into a transaction or an investment, and is produced and distributed for information purposes only.

Accendo Markets considers opinions and information contained within the research to be valid when published,

and gives no warranty as to the investments referred to in this material. The income from the investments referred to may go down as well as up,

and investors may realise losses on investments. The past performance of a particular investment is not necessarily a guide to its future performance.

Prepared by Michael van Dulken, Head of Research