Recovery potential in UK Retail

The UK retail space was blighted in 2015 by a well-documented supermarket price war that saw the big three (SBRY, TSCO, MRW) take on each other and a common foe in the almost sickeningly worshipped discounters. Interestingly, the grocers aren’t being hit by a lack of consumer spending or disposable income since these are both growing and forecast to continue doing so (Source: Tradingeconomics.com).

So what’s changed?

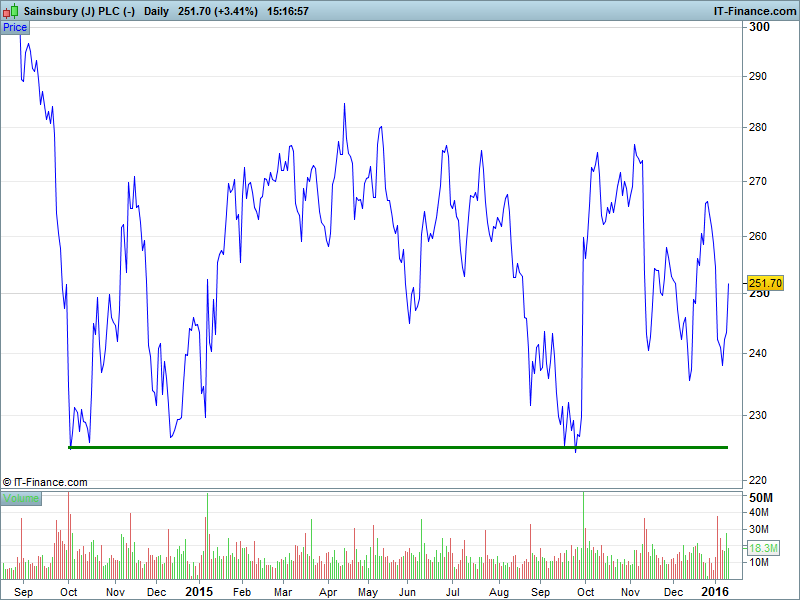

Not much – and that’s important because J Sainsbury (SBRY) has consistently outperformed its UK 100 peers in the marketplace. We’re constantly seeing investors pile into Tesco shares at every opportunity, seeing them as ‘cheap.’ Why? Because they shop at Tesco, and it’s always busy? Many have found out the hard way that this all has little to do with footfall in stores, because food prices are 2% cheaper today than they were a year ago.

This is about astute management and the recovery of market share from (fanfare please) *Aldi and Lidl*. Tesco finished the year down over 20%. Morrison’s was demoted to the . SBRY is the only UK 100 supermarket to finish 2015 in the green (up 5% to be precise), while the UK 100 index itself fell by 5%. With conditions similar to how they were last year, is it reasonable to expect SBRY to thrash the index again in 2016?