This report is not a personal recommendation and does not take into account your personal circumstances or appetite for risk.

Protect portfolio p. 4

Going short the index

An alternative hedging strategy is to go short the wider index. If you’re already holding a diverse portfolio whose performance more or less tracks that of its parent index – say the UK 100 – then shorting the index using CFDs may be more straightforward than hedging your positions separately. Using this approach, you’re able to hedge your entire portfolio in just one trade, saving a lot of dealing costs in the process.

Trading the index: An example

If you believe the UK flagship index may fall to January lows 5598 and beyond, this implies at least 250pts downside from here. Going short the UK 100 index with one CFD contract (at £10 per point) would require a £230 deposit and net you £2,500 profit if called correctly – offsetting the losses in your share portfolio. If the index rose by 250pts, however, you would of course lose that £2,500 with that loss again offset by profits in your share portfolio. In both instances, though, the trade has insulated you from market volatility.

You can limit your potential loss with the use of a stop loss. For example, you might decide to go short at £10 per point using a 100pt stop loss. If you call the direction wrong and the index rises by 100pts, you would be stopped out with a £1,000 loss on that trade, with your shares continuing to post gains beyond.

Of course it is completely up to you A) how much you go into the index (2/4/6/10/20/50/100/1000 pounds per point) B) whether you go LONG (think the index will go up) or SHORT (think the index will go down) and C) how far you place your stop loss away if at all (limiting your potential loss).

Averaging in

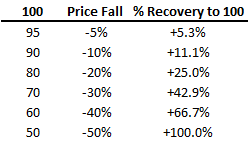

The above table illustrates how a 5/10/20% fall in price requires a bigger percentage recovery in order to achieve breakeven. While buying more as the price falls may seem counterintuitive, this is actually the practice of the contrarian trader. Contrarians buy when everyone else is selling and sell when everyone else is buying.

‘Doubling down’ or ‘averaging in’ are thus valid strategies, widely used by speculators and can prove highly successful in mitigating losses too. If the price of a held security moves down, the investor may purchase more shares at lower prices. This acts to lower the average price paid per unit – hence ‘averaging in’ – and therefore lowers the amount (in percentage terms) the price needs to recover to breakeven.

Averaging in: An example

Dave is holding 1000 shares in the blue chip company XYZ PLC (XYZ) that he purchased for £10 each. His exposure is £10,000.

An unexpected market downturn causes the XYZ share price to fall by 50% to £5.

Dave now buys 1000 more XYZ shares at the new price of £5. Since Dave now holds 1000 shares at £10 and 1000 shares at £5, the average price he paid for his shares is now (£10,000+£5,000)/(2,000 shares) = £7.50/share

His exposure has increased to £15,000.

Importantly, a 50% fall in the XYZ share price meant that a subsequent 100% recovery would be needed for Dave to break even at the original price of £10.

Dave thought this unlikely to happen, but his analysis suggested that the market should nonetheless improve in the coming days. He bought more at £5 because that lowered the average price per share to £7.50, a more realistic 50% above the new price of £5. If shares go back up to £7.50, then Dave has broken even. Phew!

If shares do indeed go on to recover to £10, then Dave stands to make back his original £10,000 investment and see his second tranche of shares return £5,000 in profit.

In the event that the share price continues to fall, however, the now greater exposure will cause losses to increase. However, Dave protects himself by placing a stop loss 10% below the price at which he averaged in. This limits any potential loss on his second position to £500 should the price continue to fall.

« Back to Category

This research is produced by Accendo Markets Limited.

Research produced and disseminated by Accendo Markets is classified as non-independent research,

and is therefore a marketing communication. This investment research has not been prepared in accordance

with legal requirements designed to promote its independence and it is not subject to the prohibition on

dealing ahead of the dissemination of investment research. This research does not constitute a personal

recommendation or offer to enter into a transaction or an investment, and is produced and distributed for information purposes only.

Accendo Markets considers opinions and information contained within the research to be valid when published,

and gives no warranty as to the investments referred to in this material. The income from the investments referred to may go down as well as up,

and investors may realise losses on investments. The past performance of a particular investment is not necessarily a guide to its future performance.

Prepared by Michael van Dulken, Head of Research