The first shots were fired overnight and responded to this morning. $68bn worth to be precise; $34bn in US tariffs on Chinese goods around midnight, and a reciprocal amount from China, just a few hours later, in retaliation. The question now is whether these opening salvos prove to be the first in a series of tariffs that escalates things towards an unwelcome trade war which destabilises global trade, jeopardises global growth and hurts global equities. Just when things were beginning to look better, a decade on from the painful financial crisis.

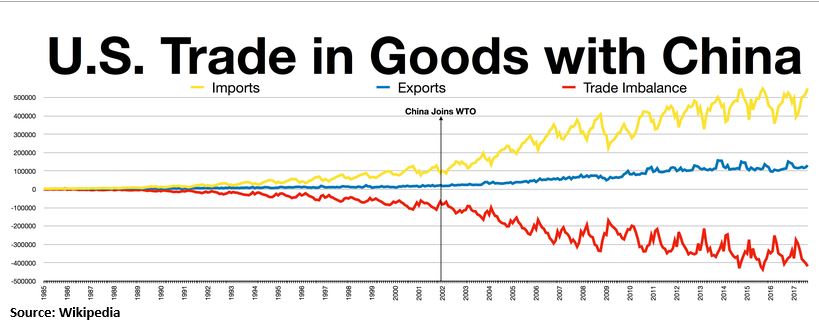

Having begun with what were, admittedly well-flagged, tariffs on $34 billion of Chinese goods, it remains to be seen how far Trump scales things up towards the $500bn figure he has been throwing around. His efforts are aimed at fixing the US trade deficit with China, punishing Beijing and delivering on his protectionist pledge to the US electorate.

To be fair, he’s only doing what he threatened to do. To be fair to China, it did say it would be obliged to retaliate. Beijing did tease us for a few hours with no immediate response, making us wonder whether they had blinked, not wanting to throw petrol on the fire. But in the end it was good for its word. Likely wanting to make sure that it was obvious that US fired first, importantly making China look like the victim.

The problem is that Trump said that if China retaliated – which it said it would, and has – that he would levy even more tariffs, which the Chinese are almost certain to match. Neither wants to lose face, perhaps even more so domestically than internationally. And Trump has talked of going as high as $500bn (the total value of Chinese exports to the US last year), trying to smoke China from abusing its ability to deliver cheaper imports which Trump claims costs jobs in the states. Even though some of the goods being targeted, are made by non-Chinese companies, perhaps even American, via JVs, with possible knock-on effects to supply chains and the US itself.

Remember also that this is on top of already introduced tariffs on metals imports to the US (to protect the steel industry), aimed at China, but which have hit the likes of Canada, Mexico and the EU. Supposed allies. Trump has also, this week, taken aim at EU cars (mostly German) which US drivers like so much. So the situation could get a lot worse. What might he target next?

That said, there are already efforts in the pipeline to get the US to abandon all tariffs on EU cars to the US, in return for removal of all tariffs on US cars to the EU. That’d put out one fire. Secondly, $34bn – call it $50bn, another $16bn are imminent – is a small percentage of Chinese exports to the US. That’s the US, not the whole world. Thirdly, Trump has a habit of kicking off negotiations from a media-friendly extreme. One that gets him the column inches and air-time he values so much. Later on though, he also has a habit of accepting more reasonable outcomes. Because it makes him look like he achieved something huge but also that he ceded ground.

My theory is that Trump goes for extreme measures knowing they appeal to his voters and get air-time, but also that there will be public uproar. The short-term backlash is worth it because he knows he will ultimately have to backtrack. At which point, those who protested are happy he ceded ground, those who supported him are happy that he tried something left-field and those he targeted feel they are not quite as worse off as they could have been.

My theory is that Trump goes for extreme measures knowing they appeal to his voters and get air-time, but also that there will be public uproar. The short-term backlash is worth it because he knows he will ultimately have to backtrack. At which point, those who protested are happy he ceded ground, those who supported him are happy that he tried something left-field and those he targeted feel they are not quite as worse off as they could have been.

With the first shots fired in the first major world trade dispute in years, you might expect it to have rocked the markets. Equities are lower, but only just, and we’re still above recent lows. We might well go lower. But investors are, as with many of the Trump stories of the last 18-months, taking this latest episode in their stride, hopeful of a market-friendly resolution, having faith that there is method in Donald’s apparent madness.

Is the calm reaction proof that this may just another case of much ado about (not-quite) nothing? After all, equity indices are still 5-20% higher than they were when he took office. The only Miner (traditionally China sensitive) down heavily this week (Glencore; -9.7%) is on internal legal issues rather than concerns over China and/or a trade war. The UK 100 is already off its lows of the day, having found support by way of 2-week rising lows.

The US President is likely to be around for at a few more years, at least, keeping financial markets and the media on their toes. Markets will remain subject to his policies, rants and twitter diplomacy (or lack thereof). In which case you and your trading/investments need someone in your corner, helping you navigate the short-term ups and downs within the longer term ups and downs. Because there will be plenty more. To see for yourself what we do daily, and how well we do it, get access to our award-winning research and let’s try and “Trump the markets” together.

Enjoy your weekend,

Mike van Dulken, Head of Research, 6 July 2018