Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

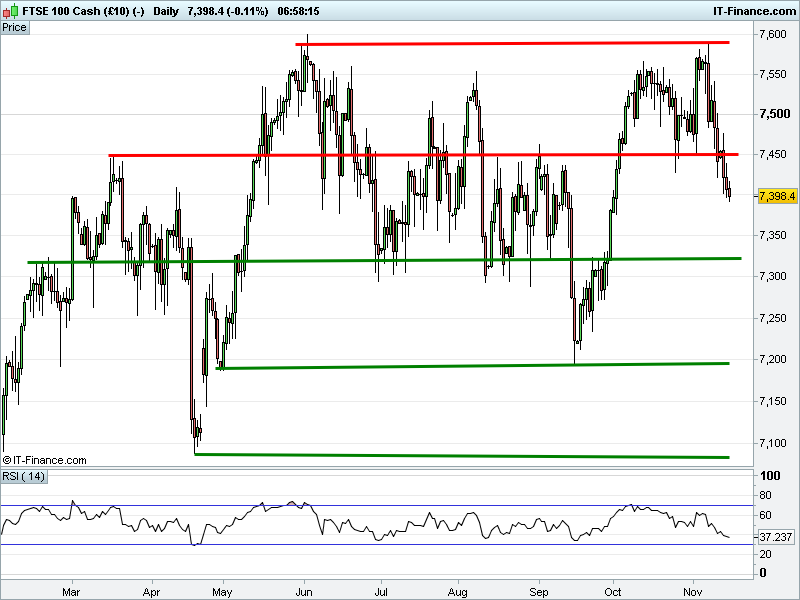

UK 100 Index called to open -25pts at 7390, to trade its lowest since 2 October after extending the 7450 breakdown on Monday. Bulls need to get back above 7410, at the very least, for any hope of overcoming the downtrend since 7 Nov. Bears are content with the prospect of a retrace towards 7300. Watch levels: Bullish 7410, Bearish 7385.

Calls for a negative start emanate from another down day in Asia as traders reduce their appetite for risk following slower Japanese Q3 GDP growth and further digestion of yesterday’s Chinese data. The latter sent metals sharply lower (iron ore futures -4.6%), resulting in another down day for Miners down under (RIO/BLT down 2-3%), which could make for a another shaky start for the sector in London.

Adding fuel to the fire, and keeping pressure on the heavyweight oil majors, will be a bullish IEA report on US oil production, which has ushered Crude Oil prices even further from recent highs dragging Asian Energy names even lower. And that’s without even mentioning geopolitics ranging from Brexit and Westminster to Zimbabwe and of course US tax reform.

In corporate news this morning Legal & General buys ETF platform Canvas with $2.7bn of assets. Cobham: 2017 Expectations Unchanged Amid Turnaround Efforts. Carillion signs letter of award with Oman Ministry of Health for £240m JV to build hospital. Experian profits fall amid decline in UK consumer service, ups dividends, expects mid-single digit organic growth for full year and stable margins. Wizz Air orders 146 new planes worth $17.2bn.

The UK CMA approves Tesco Opticians merger with Vision Express. AstraZeneca’s Asthma drug Fasenra receives FDA approval. Barratt Developments sees record start to year, expects good operating performance in 2018, with modest growth wholly owned completions. Old Mutual announces secondary offering for Old Mutual Asset management. Great Portland Estates back to profit, upbeat on London while Crest Nicholson calls for more government momentum on planning.

US equity markets closed lower yesterday as another day of losses for General Electric and lagging Energy names contributed to a negative session. The US economic bellwether fell to its lowest level in 6 years as a result of its disappointing guidance figures released Friday, weighing on the Dow Jones. Falling crude oil prices saw the energy sector weigh on the S&P 500, while the Tech-focused Nasdaq dropped 0.3%.

Crude Oil prices have fallen sharply overnight after an IEA report suggested that US Crude Oil output is set to increase dramatically in coming years, shortly before API reported a surprise build of 6.5 million barrels, at odds with estimates for a draw of 1.5 million. However, both Brent and US Crude are rallying from their lows this morning as the US dollar hits a 3-week low. Brent has moved back above $61.5 while US holds above $55.

Gold is testing resistance at $1284 after the US dollar falls sharply overnight. The precious metal remains supported at $1281 thanks to rising lows overnight, however has failed to overcome overnight highs just shy of $1284 after the greenback trades a fresh 3-week low.

In focus today will be multiple events at the UK House of Commons. The Prime Minister faces her first PMQs since the resignation of two cabinet members and the beginning of the unfolding sleaze scandal, while Brexit will likely remain a key issue throughout what is sure to be a heated session. On the subject of the latter, at the conclusion of PMQs the second day of the EU Withdrawal Bill committee stage will commence. Having voted close to midnight last night to not include access to the single and customs market during a transitional period, another late session is to be expected.

Data-wise, the top release today will be UK Unemployment and Average Earnings (9:30am). While the former is expected to remain at a 42-year low of 4.3%, the latter will be keenly watched by policymakers at the Bank of England, especially in light of yesterday’s weaker than expected Inflation prints. Expectations are for the headline figure to have retreated to 2.1% in September from 2.2%, although the ex-bonus figure is seen improving to 2.2% from 2.1%.

US Consumer Price Inflation (1.30pm) may suggest a cooling in headline prices in October (2.0% vs 2.2% pev) while the Core holds firm (1.7%),. However, Retail Sales may disappoint with no growth (0.0% vs 1.6% prev), except once Autos and Gas are excluded (0.2%) while the Empire State Manufacturing may give up ground (25 vs 30). The latest on Real Average Hourly Earnings (0.6% in Sept) may steal the show though, given its inflationary implications before a probable Fed rate hike.

US Oil inventories (3.30pm) will be in focus after the IEA said it expected US oil production to surge and demand to be lower than forecast, while US API data last night highlighted a huge 6.5m build in Crude inventories, versus expectations for a drawdown of 1.5m. Gasoline also saw a surprise build, although there was a bigger than anticipated drawdown for Distillates.

Speakers on the slate today kicks off with Chicago Fed Governor Evans (8am; panel discussion and speech about current economic conditions/monetary policy; UBS Conference) and the ECB’s Hansson, followed by ECB Chief Economist Praet (10am: closing ECB policy panel, “At the heart of policy: challenges and opportunities of central bank communication”) and the BoE’s Haldane. This afternoon (1pm) the BoE’s Broadbent speaks at the London School of Economics.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.