Macro observations

For the first time in what seems like forever, the focus for FX markets this week may move away from UK Politics. In its place, US macroeconomics looks set to take up the mantle during the week of the country’s Independence Day celebrations.

The US Dollar Basket, a trade-weighted basket of the greenback against its peers, has been trading at its lowest level since the November election of Donald Trump, while trading at 12-month lows against the Euro. This weakness has come about as multiple US data releases have been reported at softer than expected levels, bringing into question

The minutes from the 14 June FOMC meeting (Thursday; 7pm) will provide the latest look into the mindset of US policymakers, perhaps shedding more light on the trade-off between weaker data and rate hikes, and how much further disappointing releases can be tolerated when it comes to maintaining its tightening cycle.

But for the US dollar, the more pressing release this week may be US Jobs Report (Friday; 1pm), including the closely watched Non-Farm Payrolls figure. A weaker than expected release could see the Fed come under further pressure to delay hiking rates further, something which would likely weigh on the US dollar. On the other hand, a strong figure could set the dollar up for a continuation of the rally from Friday’s lows.

The Euro, after an exciting week in which rhetoric was everything, has cooled from its sharp rally of last week. Comments from ECB President Mario Draghi sent the European currency sharply higher, after investors ‘misconstrued’ a speech into believing the central banker was turning decidedly hawkish. However, after fellow members and even an official ECB press release, the single currency came off its highs as policymakers moved quickly to point out Draghi’s speech was intended to be balanced.

His comments are likely to dominate Q&A sessions with major ECB officials, including Chief Economist Peter Praet (Tuesday; 1:30pm), Governing Council member Yves Mersch (Tuesday; 7:40pm) and the hawkish Bundesbank head Jens Wiedmann (Thursday), the latter speaking ahead of the release of the ECB’s minutes from their 8 June meeting. Markets will likely attempt to pick apart the minutes to look for any indication of what circumstances are required for the ECB to begin discussing the removal of Quantitative Easing (QE), having ruled out the potential for lowering interest rates further.

Sterling, meanwhile, may find itself (relatively) calm this week, one month after the snap election that has seen the UK currency fall to a 2017 low against the Euro. Last week, hawkish rhetoric from both the Bank of England Governor Mark Carney and Chief Economist Andy Haldane helped the pound to outperform global peers, while this week, a range of macroeconomic data releases throughout the week could end up being the strongest drivers of Sterling sentiment as the political fallout from the election looks to have died down. At least, for now.

UK data includes UK Construction PMI (Tuesday; 9:30am), BRC Shop Price Index (Wednesday; Midnight), Services PMI (Wednesday; 9:30am), Nationwide House Prices (Thursday; 7am) Mortgage Approvals (Thursday; 9:30am), a significant data dump on Friday morning including Manufacturing, Industrial and Construction Output (all 9:30am) and the latest NIESR GDP Estimate (1pm).

Key data this week (Sign up here to receive our daily live macro-calendar)

—

Tuesday 4 July

US INDEPENDENCE DAY HOLIDAY – US MARKETS CLOSED

UK Economic Announcements

09:30 Construction PMI

Intl Economic Announcements

10:00 PPI (EZ)

—

Wednesday 5 July

UK Economic Announcements

00:01 BRC Shop Price Index

09:30 Services PMI

Intl Economic Announcements

01:30 PMI Services (JP)

02:45 PMI Services (CN)

8:45-9am Services PMI (European, various)

10:00 Retails Sales (EZ)

15:00 Durable Goods & Factory Orders (US)

19:00 FOMC Minutes (US)

—

Thursday 6 July

UK Economic Announcements

07:00 Nationwide House Prices

09:30 Mortgage Approvals & Consumer Credit

Intl Economic Announcements

07:00 Factory Orders (DE)

08:30 Construction PMI (DE)

09:10 Retail PMI (DE, EZ, IT, FR)

12:00 MBA Mortgage Applications (US)

12:30 ECB Minutes (EZ)

12:30 Challenger Job Cuts (US)

13:15 ADP Employment Change (US)

13:30 Weekly Jobless Claims (US)

14:45 PMI Services (US)

15:00 ISM Services (US)

16:00 Oil Inventories (US)

—

Friday 7 July

UK Economic Announcements

09:30 Manufacturing & Industrial Production, Construction Output

13:00 NIESR GDP Estimate

Intl Economic Announcements

01:00 Real Wages (JP)

06:00 Leading Index (JP)

07:00 Industrial Production (DE)

13:30 Non-Farm Payrolls, Unemployment (US)

18:00 Baker Hughes Rig Count (US)

GBP/USD (‘Cable’)

Technicals

- Failed to notch fresh 2017 high after strong rally above key $1.30 level. Back to support?

- Stochastics indicators show bearish cross in overbought level

- Momentum positive but falling from highs

- Directional indicators converging bearishly

GBP/EUR

Technicals

- Rallied from 2017 lows close to $1.125 to break out from June falling highs resistance

- Stochastics approaching overbought level

- MACD histogram at highest level since April

- Directional indicators converging bullishly

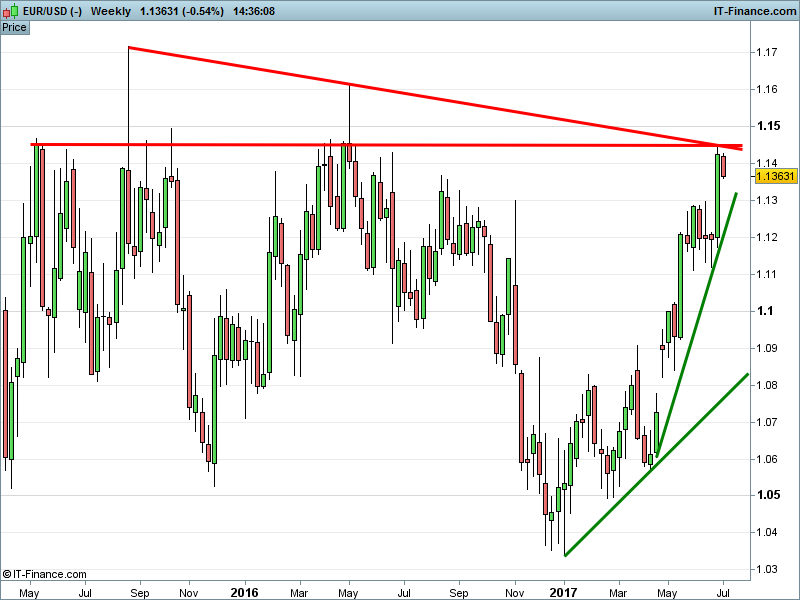

EUR/USD

Technicals

- Euro falling from duo of resistance at 12-month highs. Bounce or break at $1.13 support?

- Stochastics indicators show bearish cross in overbought level

- Momentum positive but coming off highest levels

- Directional indicators converging bearishly

For information on deliverable FX, including how you can save thousands on currency exchange, put in a call to our trading floor on 0203 051 7461. It’s all part of the service!