Macro observations

A duo of market holidays in Asia and the US has meant it’s been a quiet start to the week. By Friday, however, the peace will be shattered as a raft of macroeconomic data, events and speakers will all contribute to an exciting week.

Heading up this list will be the minutes from the US Federal Reserve’s January FOMC meeting. While policymakers decided to leave rates unchanged at Janet Yellen’s final meeting as Chairwoman, increasingly hawkish rhetoric emerging from the central bank in recent weeks has set markets up for a March rate hike. And although the market turbulence triggered by hotter-than-expected inflation took place after the meeting, policymakers’ views on what they expect from inflation in 2018 will be key in analysing what will come next.

Markets are fully priced in for a March rate hike, yet the dollar remains close to 3-year lows. An openness to hiking rates faster than expected may help to lift the dollar from its doldrums as the Fed’s peers catch up with monetary policy normalisation.

Further clues to policy could be offered this week by a series of speakers from the FOMC, including the NY Fed’s Dudley (Thursday 3pm; Friday 3:15pm), Atlanta’s Bostic (Thursday 5:10pm), Cleveland’s Mester (Friday; 6:30pm) and San Francisco’s Williams (Friday; 8:40pm).

Sterling traders this week will have to digest a range of top tier data releases.

Starting on Wednesday, UK Unemployment and, more importantly, Earnings (both 9:30am) will be highly scrutinised by traders. With Unemployment expected unchanged at a multi-decade low of 4.3%, Wage data will be the pick of the release. Despite expected unchanged at a 9-month high of 2.5% for a third consecutive month, an uptick could allow the BoE to hike rates without concern about a detrimental impact on consumers. A weak print, on the other hand, presents further quandary and could see the pound wobble.

It’s a similar story on Thursday as the second estimate of Q4 GDP and Trade Balance prints are released (both 9:30am). Once again, expectations are for there to be no change to the GDP print, however any deviation could have a major impact on Sterling.

Furthermore, an appearance from Bank of England Governor Mark Carney at Regents University on Monday evening (6:45pm) may provide some clarity on the timing and pace of BoE rate hikes following a more hawkish than expected policy meeting a fortnight ago, which would likely see the Pound react.

Euro traders will have to wait a little longer for their major drivers, with the exception of Tuesday’s ZEW Surveys and Consumer Confidence prints, as Thursday’s ECB minutes and Friday’s Inflation print headline proceedings.

Whilst the minutes are likely to have less of an impact than their US equivalent on Tuesday – predominantly due to the central bank’s pre-conceived policy plan – it may offer some further insights into the ECB’s view on a strong Euro.

Eurozone Inflation (Friday, 10am) may be a final estimate, but as with the majority of UK data this week, a deviation from the previous print and expectations could warrant a knee-jerk reaction. Especially given the ECB’s ever-increasing hawkish tilt.

There’s also the aforementioned ZEW Survey and Consumer Confidence prints (Tuesday, 10am and 3pm, respectively). The former is seen retreating from a 6-month high to a 4-month low, while the latter is expected to be confirmed at a 17-year high and withing touching sdistance of its all-time best print from 2000.

Other major macroeconomic data releases this week include German GfK Consumer Confidence & PPI (Tuesday; 10am), UK CBI Industrial Trends Orders (Tues; 11am) a range of European Manufacturing & Service PMI Prints (Wednesday; 8-9am) before the equivalent US print (Weds; 2:45pm), US Existing Home Sales (Weds; 3pm), German IFO Surveys (Thursday; 9am), UK CBI Reported Sales (Thurs; 11am), US Kansas Fed Manufacturing (Thurs; 4pm) and German Q4 GDP (Friday; 7am).

Key data this week (Sign up here to receive our daily live macro-calendar)

—

Tuesday 20 February

UK Economic Announcements

11:00 CBI Industrial Trends Orders

Intl Economic Announcements

07:00 GfK Consumer Confidence & PPI (Germany)

10:00 ZEW Surveys (Eurozone & Germany)

15:00 Consumer Confidence (Eurozone)

—

Wednesday 21 February

UK Economic Announcements

09:30 Unemployment & Wages, Public Sector Net Borrowing

Intl Economic Announcements

00:30 Manufacturing PMI (Japan)

08:00 Manufacturing & Services PMI (France)

08:30 Manufacturing & Services PMI (Germany)

09:00 Manufacturing & Services PMI (Eurozone)

14:45 Manufacturing & Services PMI (USA)

15:00 Existing Home Sales (USA)

19:00 FOMC January Meeting Minutes (USA)

—

Thursday 22 February

UK Economic Announcements

09:30 Q4 GDP & Trade Balance

11:00 CBI Reported Sales

Intl Economic Announcements

07:45 CPI & Business Confidence (France)

09:00 IFO Surveys (Germany)

15:00 Conference Board Leading Index (US)

16:00 Kansas Fed Manufacturing (US)

23:30 CPI (Japan)

—

Friday 23 February

Intl Economic Announcements

07:00 Q4 GDP (Germany)

10:00 CPI (Eurozone)

GBP/USD (‘Cable’)

Technicals

- Cable is narrowing between $1.38 rising lows support and post-Brexit highs of $1.434

- Will it breakout to fresh post-Brexit highs or fall back to lows of $1.345?

- Momentum turned positive for first time in a fortnight

- RSI remains above 50 however off best levels

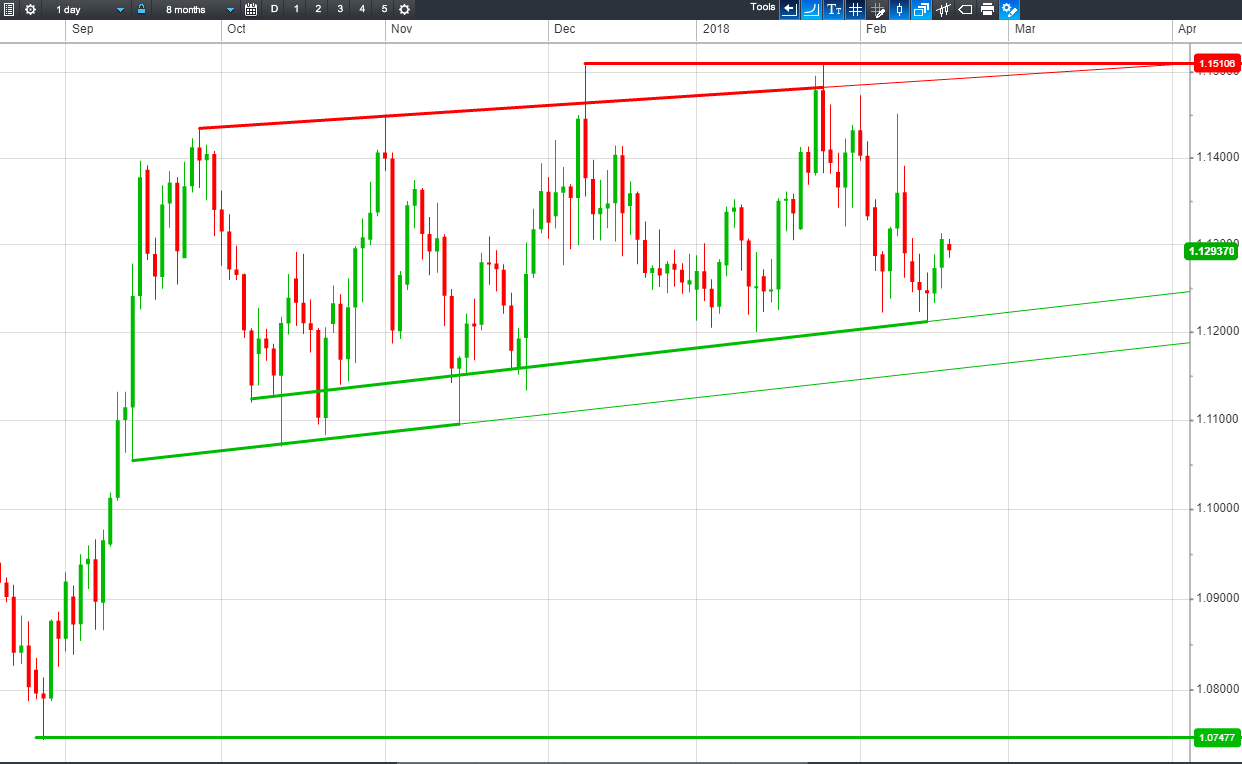

GBP/EUR

Technicals

- Sterling continues to trade in shallow rising channel between €1.12-€1.15.

- Will it break down from channel floor or bounce form channel floor to return to channel ceiling?

- Momentum approaching zero from negative

- RSI remains bearishly stuck below 50, pressured by falling highs resistance

EUR/USD

Technicals

- The Euro has retreated from resistance at $1.253

- Is this a bearish flag to $1.232 or will it recover from support around $1.24?

- Momentum turned positivefrom its lowest level since September

- RSI has turned back from its rally towards overbought

For information on deliverable FX, including how you can save thousands on currency exchange, put in a call to our trading floor on 0203 051 7461. It’s all part of the service!