Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

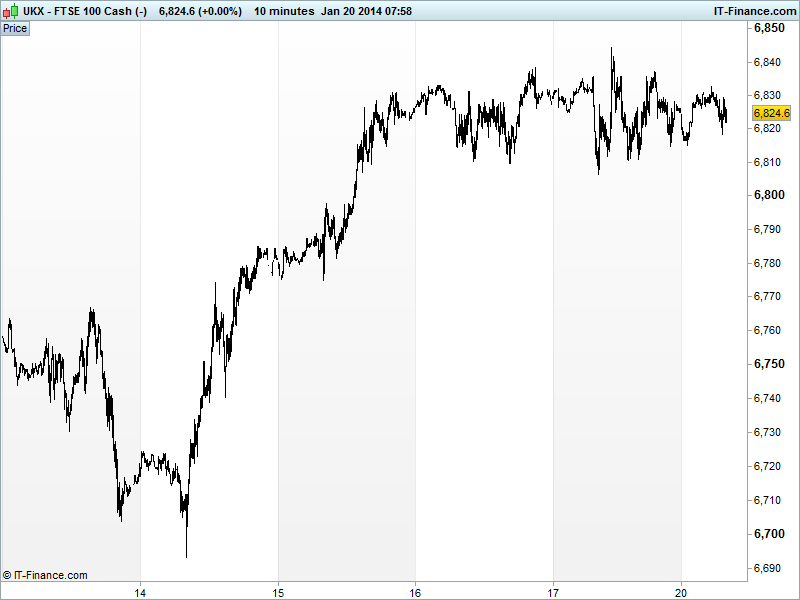

UK 100 called to open -5pts at 6820, still holding up within its new 6800-6840 sideways range, although further advances hindered this morning by the combination of mixed US macro data and Q4 results and a surprise weekend profits warning by investment bank major Deutsche Bank due to weaker fixed income revenues (as we saw with US banks), valuation adjustments and legal charges.

Sentiment impacted by mixed US close on murky macro data (Housing + Uni of Michigan) but well-received Q4 results from Morgan Stanley, dovish ECB comments and possibility of EU raising its growth forecasts, but overnight data showing Chinese GDP slowed in Q4 which maintains concerns about the possibility of a hard landing as reforms eat into domestic and global growth.

Nonetheless, weakness limited thanks to Chinese GDP coming in slightly ahead of expectations and the figure for the full year 2013 matching that of 2012, and while Asian equities week (Shanghai composite below 2000) there was an element of relief that growth was no weaker. Japan’s Nikkei weighed down by JPY strength and the Nintendo profits warning.

In fact the FT is highlighting some broker research that suggests we should not fear China’s gradual slowdown as imports of Aussie commodities are still climbing. Despite this, Australia’s ASX is in the red this morning despite the weak AUD with the prospect of the shift from investment to production cycle seeing pressure from reduced demand and profitability.

After the China GDP data, watch for the reaction by the UK listed miners, which had a strong end to last week and were some of the best gainers over the week on US growth optimism.

Other data overnight showed decline in Chinese business confidence, industrial production and investment and Retail sales. In Japan, Industrial Production was weaker than expected although Machine Tool Orders accelerated. In Germany this morning, Producer Prices rebounded which may go some way to relieving Eurozone dis-inflation fears.

In focus today, the macro data calendar is unfortunately rather sparse in account of many US markets being closed for the US holiday Martin Luther King Day.

In FX, the USD index remains strong up at 81.3 helped by macro data and hawkish Fed comments. GBP/USD of worst levels of 2014 near 1.63, but still shows falling highs form 2 Jan. EUR/USD still below 1.355, and below the trendline of rising lows from early July. USD/JPY back up above 104 while AUD/USD holding below 0.88 recent breakdown.

Gold rallied back up above $1250 despite stronger USD, as safehaven demand is revived on fears that slower China growth will have a knock-on to global growth. Potential for 1250 to revert to support. Uptrend from end 2013. Next hurdle just shy of $1270 in mid-December.

After perking up late last week, Oil holding around same levels Light Crude $94 and Brent $106 although potentially held back by Chinese industrial data.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – all part of the service.

Overnight Macro Data: (Source: Reuters/DJ Newswires)

- UK Rightmove House Prices Improved

- CN GDP Beat, slowed

- CN Industrial Production Miss, slowed

- CN Retail Sales In-line

- CN Fixed Asset Investment Miss, slowed

- JP Industrial Production Miss, slowed

- JP Machine Tool orders Slowed

- DE PPI Beat

See Live Macro calendar for all details