Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

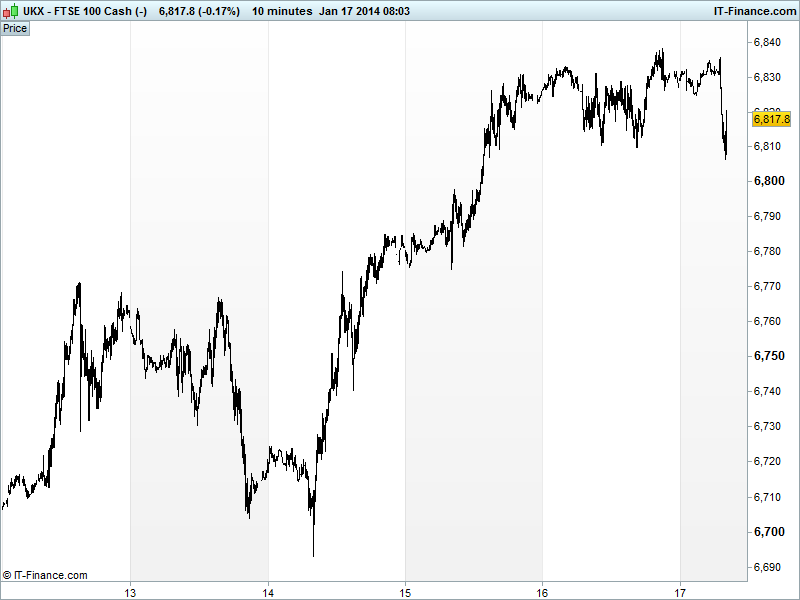

UK 100 called to open -5pts at 6810, dented by news of a profits warning from Royal Dutch Shell (RDSb) which makes up a significant 7.5% of the index. Otherwise we are holding 6010 support from yesterday after venturing as high as 6840 overnight. After a positive weak, could we see weakness test the recent breakout at 6775?

US stocks closed in the red held back by a results miss from Citigroup and uncertainty from Goldman Sachs denting the financials and mixed US macro data (inflation in-line, jobless worse, housing worse, Philly Fed headline better but new orders and stocks worse, Chicago PMI revised up). After US markets closed, tech giant Intel disappointed with a revenues beat which but profits miss suggested a still ailing PC market

After all the Fed member comments this week outgoing Chairman Bernanke said he doesn’t believe a large portion of the FOMC questions the efficacy of QE. He also referred to inflation not being a big risk (so not expecting dis-inflation?) and said the Fed is vigilant for bubbles. Note the he US government $1.1tn funding bill has received Senate approval which will remove the threat of a government shutdown for the next 8 months.

In Asia, stocks are mostly lower reacting to the US given and after Japanese consumer confidence fell unexpectedly further, the JPY strengthened as the USD weakened and despite the Abe government raising its overall view on the economy for the first time since September. China saw a good first IPO in 15 months and the PBOC sees positive signals, but equities weak.

In Europe, the big news is the European Parliament putting a spanner in the works by challenging the legality of the Eurozone bank rescue fund. Having toured Europe recently, US treasury secretary Lew also said it is not big enough!

The ECB’s Coeure has revived talk of negative deposit rates if required while Noyer said European growth showing signs of improvement. Ratings agency Fitch has affirmed the Netherlands at AAA (negative outlook) while peer S&P upgraded Portugal (still negative, but less so.)

In focus today we have a fairly light calendar although given the reaction to the banks results yesterday the update from Morgan Stanley will be keenly watched, as will those from General Electric and Schlumberger. Elsewhere we have UK Retail Sales seen solid in December, although annual growth accelerated, however, the poor Christmas updates from many UK names must be borne in mind.

In the US, after yesterday NAHB housing price slowing, US Housing Starts and permits are seen weak in Dec. Industrial Production seen growing, but slower in Dec, while Capacity Use up. To close the week, Uni of Michigan Confidence is expected to have gained a point in Jan.

In FX, the USD index is a touch weaker, but holding around 81 after mixed data ad results and but hawkish Fed comments. GBP/USD still weakening now down below 1.635 while EUR/USD found support at rising lows from July at 1.36.

Gold stuck around $1240 as index USD index hovers, struggling to do any better than $1250 but still in uptrend from end 2013. After perking up yesterday, Oil holding around same levels Light Crude $94 and Brent $107.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – all part of the service.

Overnight Macro Data: (Source: Reuters/DJ Newswires)

- JP Consumer Confidence Miss

- JP Nationwide Dept Store Sales Growth but slowed

See Live Macro calendar for all details

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Spectris expects lower 2013 operating profit

- John Menzies distribution MD McIntosh to leave

- Aviva forms JV with Indonesia’s Astra International

- Stobart says underlying profitability from Sept. 1 has continued

- FirstGroup says trading in line with management expectations

- Shell warns of “significant” profit miss

- T Clarke says trading in line with its expectations

- Shire disposes of diabetic leg ulcer treatment Dermagraft