Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

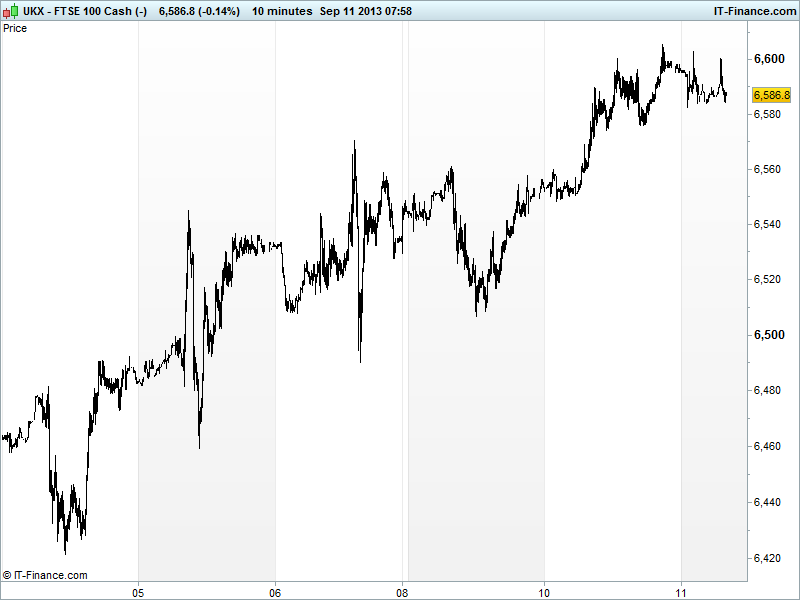

UK 100 called to open -5pts this morning at 6590, having tested but failed at the 6600 level several times yesterday and overnight. Geopolitics still the driver, with Syria situation cooling, alongside potential tapering by the Fed next week.

Asian markets mixed-to-positive, after a US finish in the green, with sentiment still buoyed by the prospect of a diplomatic resolution to the Syrian situation after US President Obama’s national address signalled a delay to a congressional vote, noting public resistance to military intervention.

After the Obama speech a French draft UN Security Council resolution gave Syria 15 days to make a complete deceleration of entire chemical and threatens further necessary measure should it fail to comply, although Syria and Russia both reject it preferring something which places no blame on the Assad regime, with the foreign minister saying ready to surrender.

Japan’s Nikkei boosted by consumer prices going in the right direction in terms of reflation of the stagnant economy. A BoJ member expects the economy to continue its moderate recovery but noted government efforts key.

Australia’s ASX helped by a jump in consumer confidence to near a three-year high. Some Asian tech names troubled by Apple product launch which disappointed many sending the US major’s shares lower. Deutsche Bank raised its China Q3 & Q4 GDP forecasts which may help miners again after weekend data.

In Europe, focus on the potential hurdles for the financial transaction tax (FTT), and ECB’s Asmussen commenting that withdrawal of Fed stimulus is too early and must be done carefully to avoid another 1994 and ECB stands ready to act if things deteriorate. Ratings agency Fitch affirmed bailout fund ESM’s AAA rating.

In focus today we have UK Unemployment which will be key given its links to the BoE’s forward guidance. Consensus is for no change in rate but a drop in claims, however, with markets refusing to accept new governor Carney’s late 2016 timeframe for a rate hike, a deterioration in the situation could actually be what gives him and UK bond yields some respite. UK Earnings growth seen showing slower growth than in June.

In the afternoon, US Wholesale sales and Inventories are the big numbers with the both seen showing improvements in July, the former growing more quickly and the former showing a rebound.

The UK 100 chart shows test but failure at 6600 with resistance on the horizon at 6630, potentially putting a spanner in the works of the uptrend since the Syria situation emerged. Support at 6500 and 6450.

In FX, USD index static around the 81.7-82 level on reduced demand for the reserve currency and safehaven of choice as Syrian tensions ease. GBP/USD solid testing June highs just above 1.57. Resistance still possible at 61.8% Fibonacci retrace of 2013 Jan-Mar decline. EUR/USD hovering around 1.325 still which could still become support for recovery to 1.345 highs of August, should USD remain under pressure.

Gold still under pressure testing trendline of rising support from end June at $1355. Safehaven demand eased on reduced geopolitical tensions surrounding Syria. Potential for rebound to $1400 and $1450 and continuation of rising channel. If break below support, downside to $1300.

Oil off worst levels after Syria intervention fears faded. Brent Crude a dollar higher at $111.5, but well off recent $116.5 highs. US light Crude 50c higher at $107 well off recent $110.5 highs. Airlines liking cheaper fuel.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – all part of the service.

Overnight Macro Data: (Source: Reuters/DJ Newswires)

- JP Domestic CGPI In-line

- JP Manufacturing & Industrial optimism Improved

- AU Westpac Consumer Confidence Improved

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Sports Direct posts sales rise as UK 100 debut nears

- Kingfisher first-half profit edges lower in tough markets

- Barratt Dev profit jumps 74 pct, says housing recovery spreading beyond London

- African Minerals says settled claims raised by Shandong Iron & Steel Group