Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

UK 100 called to open +10pts this morning at 6555 with Asian markets higher following positive weekend data from China (strong trade, benign inflation) and Japan (GDP revised higher) which offset the disappointment of Friday’s weaker than expected US Non-farm payrolls number (169K v 180K est, negative revisions for July and Jun, and low participation).

Asian data served to douse speculation that the Fed will announce tapering of its QE3 programme next week in response to improving economic data and continued concerns over Syria with Russia suggesting it would maintain current support for Assad in the case of military intervention.

Japan outperforming on Q2 GDP revised sharply higher (0.9% vs. 0.6% prev), with key investment metric strong, even if GDP was a touch below expectations and strengthens the possibility of a sales-tax hike which could impact domestic consumption (decision 1 Oct), and Tokyo winning the 2020 Olympics bid.

Australia in the green after conservative Tony Abbot won a landslide general election, ousting Labour’s Kevin Rudd after 6 years and installing a Liberal-National coalition. Confusion on Fed tapering abound but GDP surprises were for Q2 (end-June) while jobs data more recent. We still expect a delay until later in the year, all designed to keep a lid on too much bullishness.

Better China trade data, notably exports, also helping sentiment alongside inflation adding to optimism of a solid recovery with CPI cooling a touch (stimulus working, less need for cooling measures) and PPI not as weak as July (price declines of goods leaving factories recovering).

In focus today, in an otherwise quiet session for data, we have Eurozone Sentix Investor confidence seen improving. Later in the week watch for UK house prices, seen continuing their march higher. More numbers from China (Industrial Production, Investment, Retail Sales) which are expected to confirm solidity. UK Unemployment seen adding to BoE Governor Carney’s woes on forward guidance.

Eurozone Industrial Production watched for continued signs of regional recovery. US Weekly jobless claims of interest in light of payrolls miss and uncertainty on tapering. US inflation and Retail sales seen slightly improved in August, however, Uni of Michigan Consumer Confidence seen taking another tick back from recent high.

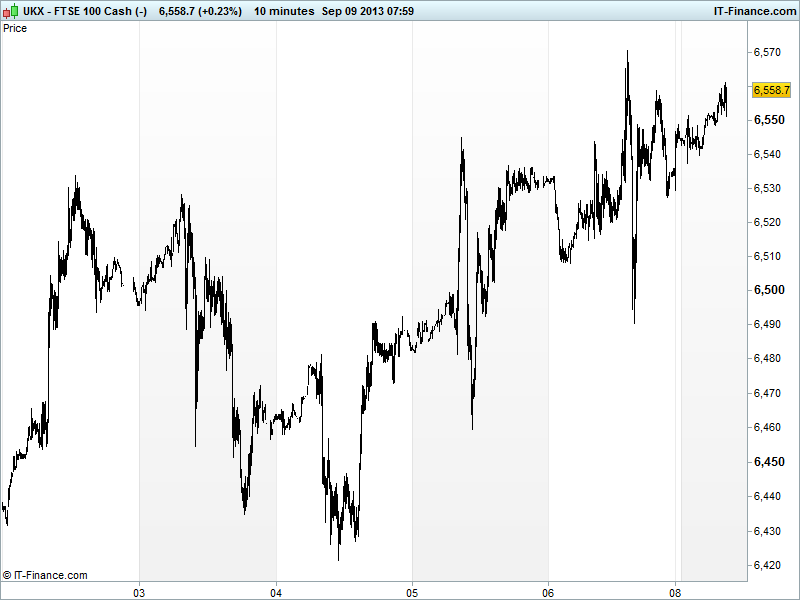

Looking at the UK 100 chart, the September recovery persists with ground being made slowly and after the breakout above the falling highs of August. Support 6520 after breakout and thanks to rising lows, then 6450 from Rising lows from mid-August. Major resistance at 6660 from July struggle, although a revisit of 6700 could materialise.

In FX, USD index fallen back towards 82 after payrolls data where it could find support. GBP/USD bounce again off 2013 trendline but still needs to break above August highs 1.572. EUR/USD bounced on USD weakness, finding support at 1.31, but well off late August highs of 1.34.

Gold holding up just below $1400 but in off its best levels of August and in short-term downtrend with support likely at $1350. Safehaven seeking due to Syria situation still having an impact on Gold while supply concerns keeping the price of US and Brent Crude Oil up around the highs of last month.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Vodafone may fail to clinch Kabel Deutschland

- Ricardo full year profit up 31 pct

- BBA Aviation merger talks with Dubai Aerospace terminated

- Miner Lonmin appoints two Glencore Xstrata execs to board

- AB Foods earnings growth driven by Primark

- BGGroup says delays in Egypt, Norway to affect 2014 output

- Petroceltic sees FY output at around 25,000 boepd

- IGASEnergy signs deal to buy Caithness Oil

- SNR says in investment talks with several interested parties

Overnight Macro Data: (Source: Reuters/DJ Newswires)

- JP GDP Improved

- CN Trade, Inflation Better

See Live Macro calendar for all details