Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

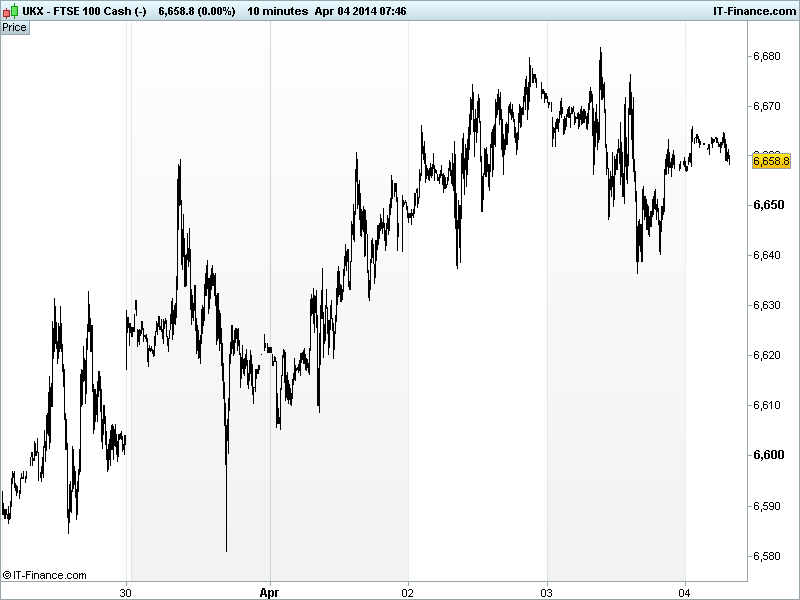

UK 100 called to open +20pts at 6660, despite the first flat/weak US close in multiple sessions after data from the world’s #1 economy failed to inspire with misses from weekly jobless claims, trade balance and Services sector sentiment readings (PMI and ISM) and defensiveness returned ahead of today’s US Jobs report and some banks pulled back Q1 GDP estimates.

The ECB left policy unchanged but alluded (again) to not being all out of options, including unconventional measures (LTRO, SMP, negative rates; within remit) to stave off disinflation (which ECB President Draghi said was a risk, again, but talked down, again) and that all council members (incl. Bundesbank’s Weidmann) are in favour of such measures should it be necessary.

In Asia overnight, optimism in check after US weakness with equities trading in tight ranges (although set for second weekly gain), with caution ahead of the Non-Farm Payrolls which is expected to show the biggest increase since November, before winter weather began hampering things. Data-wise, German Factory Orders are mixed this morning, better on the month but growth having slowed over the year.

On the geopolitical front, after a period of calm, the House of Representatives Spokesman Carney said seen no evidence of Russian troop reduction near Ukraine, while Russia has recalled its military envoy from the NATO and now sees reduced cooperation. The Fed’s Fisher estimates QE3 will end in October and that calendar based policy commitments lead to instability.

In focus today, we have Eurozone Retail PMIs which could give an idea of consumer confidence although there is no consensus and prior readings were mostly <50, bar a healthy 52 Germany.

Then it’s all about the US March Jobs report and whether 200K jobs can have been added in March, the cold weather no longer having an impact. The Unemployment rate is seen ticking back down to 6.6% (Jan’s reading), however, the Fed’s recent comments put less weight on this and more on overall progress (participation?). Any revisions will be of interest after the big ADP jump for Feb on Wednesday.

In commodities, the price of Gold has held on to yesterday’s gains and recent highs around $1285 ahead of the US jobs report, although volatility is expected when the data is released. Physical demand still being seen supporting the safehaven metal. The metal is still faced with a third weekly decline (longest since September) with expectations that the US jobs report shows the fastest growth in four months and takes us closer to the end of US monetary stimulus.

WTI Crude back up above $100/bl and Brent crude above $106/bl on concerns that talks between the Libyan government and rebels will fail to restore exports.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – all part of the service.

Overnight Macro Data: (Source: Reuters/DJ Newswires)

See Live Macro calendar for all details

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Shell’s grounded rig product of poor tow plan -U.S. Coast Guard

- Ofwat confirms enhanced status for Pennon subsidiary

- Flybe fourth quarter trading in line with expectations

- Kentz CFO to step down in May

- Workspace Group sells Bow development for 11 mln pounds

- Evraz sells Evraz Vitkovice Steel for $89 mln

- RBS appoints new finance chief from Credit Suisse

- Victoria Oil and Gas estimates Bonaberi production at 4mmscf/d by June