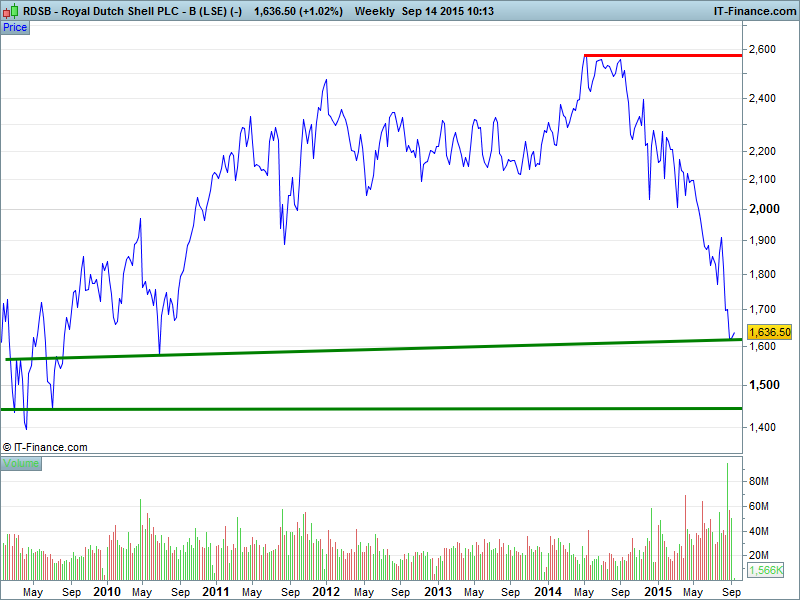

Is the Oil & Gas business set to enter a new paradigm?

Recent reports about the future of the UK’s North Sea oil & gas fields has raised alarm, compounding already present worries about the industry at large. A low oil price that doesn’t appear too keen to move higher any time soon, lower demand from an apparently slowing China and competition in the form of Shaleand its potential to bring energy self-sufficiency ever closer to the US and UK have conspired to open up a war on multiple fronts.

Stubborn oil producers are now fighting to maintain their share of the global market, but with crude prices where they are the fight will almost certainly fail to produce any winners. There’s little point in things carrying on the way they are and the competitors know it. The question is who will back down first?

One of the reasons we’re in this situation is the sheer bloody mindedness of two of the major oil producers: OPEC and the USA. While OPEC has been pumping record amounts of crude into the market for some time, hoping to squeeze out global rivals, its main competitor – the US – has remained resilient and while OPEC’s so-called ‘fragile five’ will likely continue to produce at current prices, there’s only so far you can go without paying wages before workers start taking action. We’re unlikely to see $100/barrel oil any time soon but the current state of affairs in the Oil and Gas sector cannot continue, and there are two ways in which it could correct.