Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

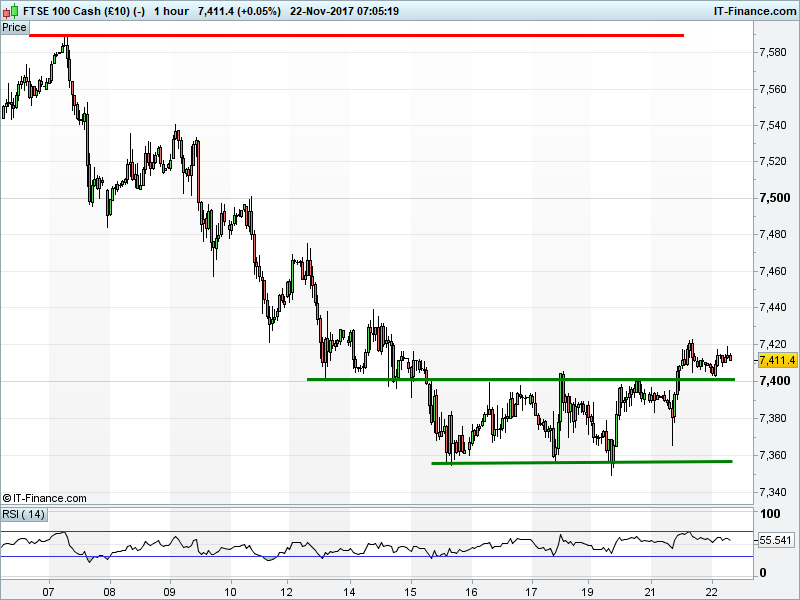

UK 100 Index called to open flat at 7410 holding above yesterday’s 7400 breakout. Bulls hope this remains supportive, a trampoline for continued rebound towards 7500. Bears are looking for any signs of weakness and a breakdown towards last week’s lows of 7355. Watch levels: Bullish 7425, Bearish 7395

Calls for a flat open come in spite of more stateside gains (and record highs) and another positive session in Asia overnight where Hong Kong’s Hang Seng hit a 10-yr high helped by earnings reports, financials and Oil rallying to help Energy following supportive US inventory data and Canadian pipeline disruption.

Metals prices are also higher, helping the Miners down-under, amid USD weakness (US holiday, dovish Yellen, tax delays), Indonesian mine-supply disruptions and hopes that Chinese output cuts will be less than expected.

In corporate news this morning GlaxoSmithKline says Juluca approved in US as first two-drug maintenance regimen for virologically suppressed HIV-1. United Utilities financial performance in-line with expectations, working towards 2020-25 price review. Thomas Cook revenues and profits jump, UK and Spain challenging but confident in FY results meeting consensus.

Sage expects acceleration in 2018 organic revenue growth, but suggests 50bp decline in organic operating margin, ups dividend. Hammerson sells 64.5% stake in Strasbourg’s Place des Halles shopping centre for €291m just above its mid-year book value.

US equity markets closed at record highs overnight ahead of Thursday’s Thanksgiving holiday, performing strongly on the back of a strong rally for the Technology sector. Unsurprisingly, the Tech-focused Nasdaq outperformed, rallying over 1% on the day, however this strength also spread to the Dow Jones and S&P 500. Apple led gains on the former, while the latter traded above 2600 for the first time.

Crude Oil prices have rallied overnight as the American Petroleum Institute reported significant drawdowns in US inventories. A 6.5m barrel draw, over three time larger than expected, has seen US Crude rally over 1% overnight to an almost 2-week high at $57.75, where it is testing resistance, while Brent Crude has rallied to a 1-week high above $63. Watch official US EIA inventories this afternoon for a confirming or dispelling of the API release.

Gold has extended its tentative recovery from Monday afternoon’s sharp sell-off, continuing climbing from 1-week lows around $1275 as the US dollar retreats from the ceiling of its rising channel. The precious metal traded an overnight high of $1283.5, just shy of yesterday’s $1285 highs, and will likely continue to be driven by the greenback throughout the day ahead of this evening’s FOMC minutes and tomorrow’s Thanksgiving holiday.

In focus today will be the UK Autumn Budget (12.30pm) and what Chancellor Hammond does or does not give away, given the fiscal constraints he faces in preparing the economy for Brexit.

Housebuilders may get a boost from policies designed to attract younger voters (stamp duty cut, Help to Buy/Build, land development), while the Chancellor may hold a card up his sleeve in the form of the usual ‘gimmes’, such as bringing forward increases to income tax thresholds that were projected for 2020. Increases in alcohol and tobacco duty would affect their relative sectors.

Prime Minister’s Questions (12pm) may also prove a lively warm up to the Chancellor’s time at the despatch box, given PM May’s travails and party divisions. Thereafter, comments from the ECB’s Villeroy (8am & 12.30pm) and the latest Fed FOMC Meeting minutes (7pm) will also be scoured for clues about monetary policy on both sides of the Atlantic.

Data-wise, it’s slim pickings in the run-up to the US Thanksgiving holiday, with US Durable Goods Orders (1.30pm) likely having slowed in October while both Eurozone Consumer Confidence (3pm) and US Michigan Confidence hold pretty much flat .

US Oil inventories have potential to deliver the draw-downs expected last week following last night’s API data, which could give oil prices another fillip, US Crude perhaps even breaking above recent $58 >2-year highs, Brent regaining November $64.5 highs.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.