Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

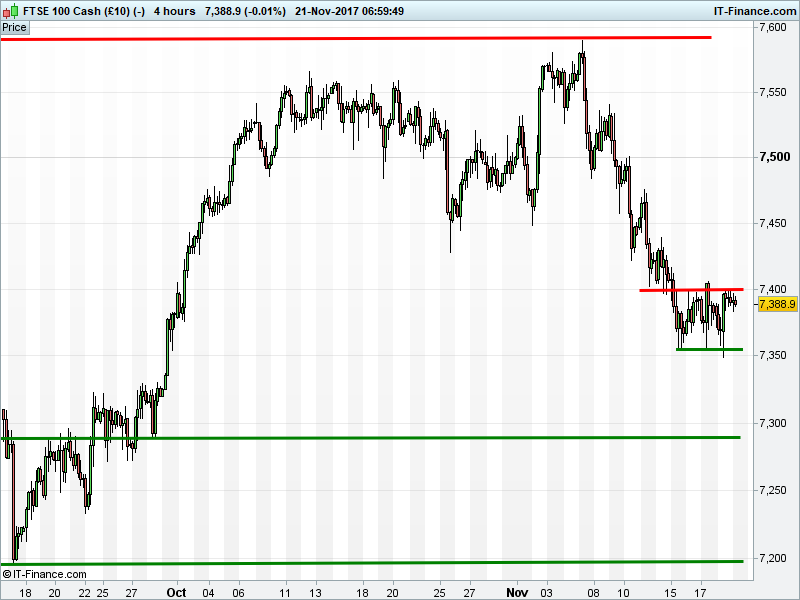

UK 100 Index called to open flat at 7390 having held sideways 7385-7400 since yesterday afternoon. Bulls hope this is a in preparation for a breakout above the bugbear 7400 level. Bears are angling for a breach of 7380, for a retrace to 7340. Watch levels: Bullish 7405, Bearish 7380

Calls for a flat open come in spite of a positive close on Wall St, and Asian trading following suit overnight to counter Monday’s weak start. Chinese insurance has been the standout performer ahead of earnings updates, while Australia’s ASX shows gains for the Miners and Energy as Oil extends its bounce. Whilst the latter may help the UK Index , a stronger GBP on the prospect of the UK unlocking Brexit negotiations with a higher settlement is also hindering.

In corporate news this morning BHP Billiton (and Vale) enter into amendment agreement in relation to Samarco dam failure for additional consultation and extension of suspension to legal proceedings and injunctions. CRH expects FY EBITDA >€3.2bn vs consensus €3.3bn. Compass Group positive on FY2018, growth and margin improvement weighted to second half, pipeline encouraging, focus on organic growth. Johnson Matthey full year guidance unchanged, ups div.

Babcock “excellent revenue visibility with 92% of budgeted revenue in place for FY18”, expects slightly improved margins in second half, confident meeting FY guidance. WPP to sell 25% stake in Japan’s ADK to Bain Capital. Kingfisher Q3 like-for-like constant FX sales -0.5% vs -0.6%e; B&Q UK/IRL slightly less weaker, Screwfix stronger, France weaker, Poland stronger; On track for FY.

Intertek full year outlook for products division remains unchanged, continue to expect robust organic revenue growth at constant FX. easyJet FY results slightly ahead of consensus, in-line with guidance. Aggreko full year guidance remains unchanged.

US equity markets closed higher yesterday as investors awaited further details about tax reform, while welcoming positive macro data. The Dow Jones outperformed, closing 0.3% higher as heavyweights Home Depot, Boeing and 3M led the way forward, offsetting Merck weakness. Both the S&P 500 and the Tech-focused Nasdaq closed 0.1% higher, the former thanks to Telecoms strength while the latter closed just shy of a record high.

Crude Oil benchmarks are edging back towards yesterday’s highs, unperturbed by continuing US dollar strength, as hopes that OPEC will extend production cuts at next week’s meeting have lifted prices from lows. Brent Crude trades back above $62 a barrel, although will have to overcome multiple resistance levels before returning to $63, while US Crude has a relatively clear rung to $57 from $56.5.

Gold suffered its worst single day drop since September as a resurgent US dollar dampened sentiment for the precious metal. Having fallen to a 1-week low just below $1275, it has since climbed to an overnight high of $1281, although has begun to turn back from intersecting resistance. Currently, the precious metal is holding just above $1280.

In focus today will be a duo of UK macro data releases before tomorrow’s Autumn Budget. Public Sector Net Borrowing (9:30am) will provide a gauge of how much the Government intends to set aside for Budget spending, especially given Chancellor Hammond’s desire to reach his self-imposed fiscal targets. Expectations are for Borrowing to have increased to £6.5bn, in line with seasonal trends from previous years. Thereafter, CBI Trends Orders (11am) are expected to return to growth having turned negative for the first time in 11 months in October.

Other data today include the US Chicago Fed National Activity Index (1:30pm), expected to tick marginally higher in October, while US Existing Home Sales (3pm) are expected to improve for the second month in succession.

Speakers of note during trading house today include a quadruple whammy of Bank of England Governors (McCafferty, Cunliffe, Saunders and Vlieghe; 10am) and the ECB’s Coeure (3pm). Note Fed Chair Janet Yellen speaks at 11pm, just a day after announcing she will step down from the board of governors once colleague Jay Powell takes over the top job.

Continue to keep an eye out for updates from Germany, where Chancellor Merkel has vowed to fight a new election rather than lead a minority government, the US with only two days to advance tax reform plans in the Senate before Thanksgiving, and, of course, any leaked details – intentionally or otherwise – of tomorrow’s UK Budget.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.