Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

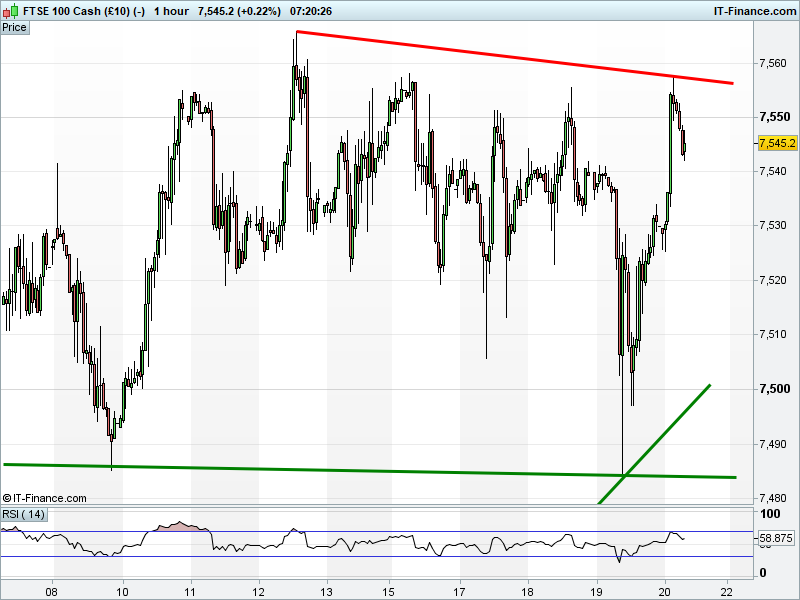

UK 100 Index called to open +20pts at 7545, having extended its rebound from 7500 to retest the 7555 highs of the week. Bulls need a break above these and last week’s 7565 peak to revisit August’s 7600 record. Bears are looking for a breach of 7540 resistance-turned-support to trigger a full retrace to 7500 rising support. Watch levels: Bullish 7555, Bearish 7540.

Calls for a positive open are again mostly attributable to GBP weakness, this after the USD popped overnight on Senate Republicans approving a budget resolution that essentially paves the way for a $1.5tn US tax cut package. This would represent the first major reform from President Trump’s administration following several stumbles, seen as supportive of US growth, Fed rate hikes and, of course, equity markets.

Down-under, Australia’s ASX outperforms, testing levels last seen in May, thanks to financials, consumer staples and a bounce for metals prices (in spite of the USD bounce). Japan’s Nikkei is flat, dented by a Nissan production scandal, but buoyed by USD strength translating to helpful Yen weakness for exporters.

UK Index corporate news includes Intercontinental Hotels sees 2017 trading in line, Q3 RevPAR +2.3%. Smiths Group extends pension de-risking via £207m bulk buy-in agreement with Canada Life. Serco COO Ed Casey to leave at year-end. Acacia Mining continues to seek further clarification and a formal proposal from Tanzanian government.

Dechra Pharma says Q1 performance in line with management expectations, with continued growth across all markets. Interserve awarded 5yr £227m facilities management contract for the UK’s Department for Work & Pensions (DWP).

US equity markets overnight recovered from Wednesday’s Tech-inspired dip, with the exception of the Tech-focused Nasdaq, finishing marginally higher at fresh record closing highs only a day after their sharpest fall in a month. The Dow Jones closed just above break-even thanks to a strong performance for insurer Travelers, while the S&P 500 benefitted from a 12% rally for Adobe, offsetting Tech weakness elsewhere after Apple fell on iPhone 8 demand concerns .

Crude Oil prices have rallied from rising lows support overnight, however remain significantly below below yesterday afternoon’s highs of $57.7 (Brent) and $51.9 (US). The US dollar could remain a key driver of sentiment today as the Trump administration looks to pave the way for tax reform, while traders await further commentary from OPEC regarding a potential 9-month extension of production cuts.

Gold has retreated overnight as US Senate passes a key budget that will allow tax reforms to be made by the Trump administration, seeing the US dollar rally to the detriment of the non-yielding safe-haven asset. After retreating from overnight highs of $1291, the precious metal is holding at intersecting support at $1282, although further US dollar strength may negatively impact sentiment.

In focus today will be any soundbites from the EU leaders summit (ex-UK) in Brussels where Brexit will be discussed after UK PM May’s efforts to break the deadlock on negotiations. Thereafter, we are a step closer a Saturday cabinet meeting in Madrid which could follow through on the threat of re-imposing direct rule on Catalonia following the autonomous region’s referendum.

Data-wise the Eurozone Current account which is expected to show a smaller August surplus, reversing much of its recent rise, back around the 2017 average, with a potential knock-on for the EUR. UK Public Sector Borrowing is forecast higher in September, continuing to increase again following the mid-year seasonal improvement.

The only speakers of note outside the EU are the Fed’s Mester (7pm) and Chair Yellen (Saturday morning; 12:30am). Mester, who will become a voting member in 2018, will discuss ‘The Future of Global Finance: Populism, Technology and Regulation’ in New York, while Yellen delivers a lecture on ‘Monetary Policy Since the Financial Crisis’ in Washington.

US companies reporting today: oil services giants Schlumberger and Baker Hughes, retail bank Citizens Financial (owned by RBS until 2015) and Industrial behemoths General Electric and Honeywell. The most interesting, however, may in fact be Procter & Gamble, especially after poorly received updates from Unilever, Reckitt Benckiser and Nestle in Europe.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.