Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

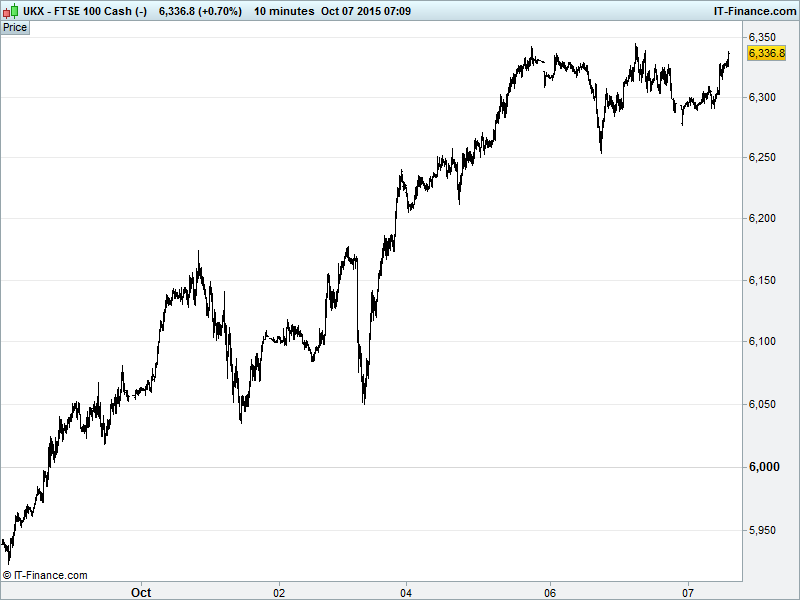

UK 100 Index called to open +25pts at 6350, managing to hold up above the 6250 breakout, taking a pause for breath after sharp gains from end-September lows 5870. The ability to stay above the 6300 September highs and Jan 2015 lows is positive and, following this breather, we could see upside towards 6600 June falling highs. Unchanged watch levels: Bullish 6360, Bearish 6290.

Another positive opening call comes despite a mixed finish by US bourses (healthcare down) after the IMF cut global growth forecasts (but not China?) and thanks to gains across the board in Asia overnight on the back of an oil price extending its recent bounce and breaking out of a 1-month sideways shift and a general bounce by commodities.

Asian stocks higher helped by Samsung Electronics delivering better than expected Q3 profits guidance helped by strength in semiconductors which has offset weakness in smartphone. Keep an eye on chip architect ARM Holdings (ARM) this morning given its exposure to both spaces.

Japan’s Nikkei is higher (energy leading thanks to oil rally) despite the BoJ holding fire on more stimulus. With investors desperate for the global easy money policy song to play longer (US, UK) and louder (BoJ, ECB), the delay is not worrying markets which have just increased the odds of recessionary signs forcing the central bank to act on 30 Oct.

On the stimulus front, note more poor German data (Industrial Production after Factory Orders) for August, before we get any impact from the VW September emissions cheat fiasco, is likely to intensify calls for the ECB to confirm prolongation/expansion of its QE programme to foster regional growth and avoid deflation.

On the corporate front, note AB Inbev’s (BUD) improved 4215p cash bid (up from 4000p) for SABMiller (SAB) while Tesco (TSCO) results show that H1 profits halved for the troubled grocer.

In focus today: UK Industrial Production seen losing ground in August, although Manufacturing may have picked up. Thereafter, we have the UK PM David Cameron speaking at the Tory party conference with an apparent focus on affordable house-building (watch the house-builders). The German and French leaders Merkel and Holland speak mid-afternoon, and Fed’s Williams and IMF’s Lagarde tonight.

The Oil price is extending its bounce to $6, its longest positive run since April as US API data showed stockpile declines, this ahead of EIA data this afternoon. Additional help from comments by the Royal Dutch Shell (RDSb) CEO about potential for current market adjustment (operational + capex cuts, etc) to lead to a future price spike and the OPEC chairman similarly seeing price rises after a 20% cut in 2015 spending. Note Middle East geopolitics helping too.

Gold has continued to break higher from the bullish flag pattern we had identified to test $1150 thanks to hopes of US rate hike delay weakening the USD. Importantly, this takes us above the long term (8-month) trend-line of falling resistance which could allow for completion of the flag pattern around $1170 Aug highs.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires/Bloomberg)

- Tesco shows signs of recovery after profit collapse

- AB Inbev revises proposal to acquire SABMiller

- Wood Group wins automation project for Tengiz field, Kazakhstan

- Diageo sells interest in GGBL to Heineken

- Bowleven names William MacDonald Allan as chairman designate

- Tethys Petroleum says Nostrum Oil withdraws proposed takeover offer